Telematics is no longer a buzzword on the horizon. It is the infrastructure behind the commercial auto insurance industry’s shift from reactive risk management to proactive loss prevention. And for insurers, brokers, and fleets navigating one of the most challenging markets in decades, understanding telematics is no longer optional.

This guide will cover everything needed to better understand this technology—what telematics is, how it works, what telematics data captures, and how the commercial auto insurance ecosystem uses it to reduce violations, prevent crashes, and improve loss ratios.

What is Telematics?

Telematics is the technology that continuously collects, transmits, and analyzes vehicle or driver behavior data. The word itself combines “telecommunications” and “informatics”, a fitting description for a technology that pairs connected devices with data intelligence.

At its core, a telematics system uses a physical device or a smartphone application to capture data points such as speed, location, and braking patterns, which are then collected on a centralized platform. Many of these devices and platforms are built and operated by companies known as telematics service providers (TSPs).

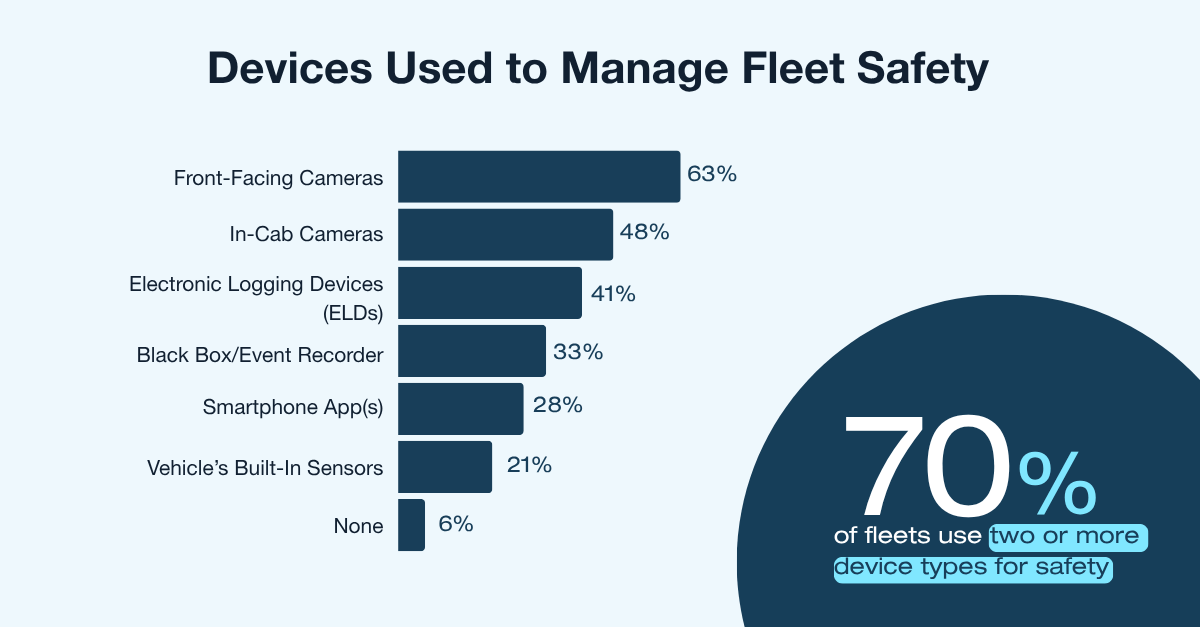

Today, commercial fleets utilize multiple TSPs simultaneously. SambaSafety’s 2025 Telematics Report found that in 2025, 70% of commercial fleets use two or more devices to manage fleet safety. Yet despite that widespread adoption, only 30% of fleets actively share that data with their insurer. More on that later.

For the commercial auto insurance industry, telematics goes beyond GPS tracking. It has become a foundational part of risk intelligence, replacing point-in-time snapshots with continuous visibility into the behaviors that lead to losses.

What Is Telematics in Insurance?

Telematics in insurance refers to the use of collected data to identify and address driver risk throughout the policy lifecycle. Historically, underwriting has relied on data from past claims, irregular MVR pulls, and self-reported information to determine policy premiums.

Telematics for insurance flips this concept on its head by introducing a continuous, behavior-based layer of intelligence that reflects what’s happening on the road. In commercial auto, telematics serves two connected purposes:

-

Risk assessment

-

Risk reduction

For risk assessment, telematics data can help insurers, specifically underwriters, obtain a more up-to-date and complete picture of driver risk throughout the policy lifecycle. Rather than relying on annual snapshots that can miss violations or crashes, insurers gain visibility into the risk patterns that translate into claim likelihood.

In a risk-reduction scenario, telematics data enhances an insurer’s ability to proactively prevent losses. When fleets share telematics data with their insurer or broker, risk control teams can connect those insights to targeted training and coaching—helping policyholders make meaningful behavioral changes.

This dual function makes telematics data so valuable in a commercial auto insurance landscape already under a lot of pressure. Not only does it help insurers better understand risk, but it also helps the entire ecosystem work together to reduce it.

How Does Telematics Work?

When you think about the ins and outs of a telematics system, things can get complex quickly. At a high-level, a telematics system has three core components.

First, the in-vehicle device or sensor. Most commercial fleets use a hardwired or plug-in device that connects to the vehicle’s internal computer. The telematics device captures the vehicle’s data on speed, braking, mileage, and trip tracking. With the prominence of in-cab cameras, this telematics data now includes video context to behavioral events—a pivotal capability as nuclear verdicts make documented evidence extremely valuable.

Common telematics device types include:

- Hardwired OBD-II device installed directly into the vehicle

- Plug-in devices for fast deployment across large fleets

- In-cab cameras that capture video

- Smartphone-based applications that use device GPS and motion sensors

Next, the data transmission layer. As data is captured by the device, it’s transmitted to a cloud-based platform. This is what powers continuous monitoring and enables seeing what’s happening across a fleet without waiting for a driver to self-report or for a renewal cycle to arrive.

The analytics platform is the third and most consequential component. Raw data on its own isn’t entirely actionable. But within an analytics platform that normalizes, scores, and contextualizes that data, insurers can make informed decisions. That’s where telematics becomes a risk intelligence engine that surfaces patterns and alerts on risk before it materializes into a claim.

For insurers and brokers, the analytics layer is where telematics data earns its value. Here are key capabilities to look for:

- Normalized data across multiple TSPs

- Driver-level risk scoring that’s consistent across a book

- Automated alerts tied to intervention

- Portfolio dashboards that surface trends across accounts

What Data Does Telematics Capture?

Telematics can generate billions of data points—but there are key variables that commercial auto insurers tend to pay attention to: speeding, harsh braking, distracted driving, route patterns, and hours of service.

Speeding is prevalent. SambaSafety’s 2025 Risk Report shows speeding accounts for nearly 40% of all major violations in the U.S., making it a crucial telematics signal of a driver’s risk profile. Harsh braking or rapid acceleration can indicate following too closely or inattentive behavior. Together, all three of these signals can paint a picture of how a driver operates behind the wheel.

Distracted driving adds another critical dimension. Detected through in-cab cameras or phone motion sensors, distraction contributed to 3,275 fatalities in 2023 and remains one of the most underreported risks in commercial fleets.

Beyond these vital behavioral variables, telematics can also capture operational data that is necessary for a commercial environment. Idle time, route patterns, and hours-of-service compliance through electronic logging devices (ELDs) provide essential insights to safety program managers and risk control to understand the full context behind a driver’s behavior patterns.

Each signal provides useful context individually. Together, they contribute to a continuous, complete driver risk profile that gives insurers and brokers a far more accurate and actionable picture of exposure than any single point-in-time assessment.

Why Telematics Matters and is Meeting the Moment

In 2024, underwriters faced $4.9 billion in losses, and as of late 2025, a reported 58 consecutive quarters of premium increases have done little to reverse the trend. With nuclear verdicts becoming a regular occurrence and rising repair costs affecting claim severity, the traditional risk management toolkit is no longer meeting the moment.

Retrospective tools to evaluate risk, such as annual Motor Vehicle Record (MVR) pulls or periodic audits, reveal what has already happened, not what is happening or about to happen. Telematics in insurance changes the equation entirely by providing visibility into risk variables that can indicate future losses.

As SambaSafety CEO Matt Scheuing noted, “We’re at a pivotal moment where we can move from reactive risk management to proactive risk prevention.”

That pivot is what telematics helps make possible.

For insurers and brokers, telematics data—when aggregated across providers and normalized into consistent risk metrics—becomes a competitive advantage instead of an operational burden. How?

The ability to prioritize which policyholders need attention and deliver scalable risk consulting demonstrates measurable impact rather than anecdotal observations. Giving underwriters confidence to price accurately and drive better outcomes is an advantage worth seizing.

Closing the Telematics Adoption Gap

One of the most striking findings from SambaSafety’s 2025 Telematics Report reveals a fundamental communication breakdown that is slowing industry progress. Seventy-five percent of commercial insurers believe convincing fleets to share telematics data is their biggest adoption hurdle. Yet 79% of fleets that aren’t sharing data say the reason is simple. They were never asked.

The infrastructure is already largely in place. With 88% of fleets already using telematics devices for safety, the barrier to data sharing isn’t technical; it’s the dialogue about how the data will be used and the value each party will get out of it.

For commercial auto insurers, the moment to lead the conversation is here. Transparency about how data will be used, and the value it returns to the fleet, is what converts participation from obligation into partnership.

The Role of AI in Amplifying Telematics Intelligence

Telematics generates enormous volumes of data. Artificial intelligence (AI) is what transforms that volume into scalable intelligence, and its impact on telematics for insurance is only beginning to materialize.

AI applied to telematics data enables capabilities that were not possible at scale just a few years ago. Predictive risk scoring can automatically surface which policyholders present the greatest emerging exposure, allowing risk control teams to prioritize interventions without manually reviewing every account.

Pattern recognition identifies dangerous behavioral combinations across a book before they result in incidents, shifting loss control from a reactive function to a genuinely predictive one. And AI-driven training recommendations matched to specific violation types ensure that when interventions do occur, they are relevant, targeted, and more likely to drive lasting behavior change.

As camera adoption increases across commercial fleets, AI-driven video analysis adds another layer of precision—providing documented behavioral evidence that supports both risk control decisions and legal defense in an era of escalating nuclear verdicts.

Insurers and brokers who build their risk programs on a high-quality telematics data infrastructure today will be best positioned to leverage these AI capabilities as they mature. The insurers and brokers who build on a strong telematics data foundation today will find that advantage increasingly difficult for competitors to close.

Putting Telematics to Work Now and In the Future

The commercial auto insurance industry cannot manage risk the way it did a decade ago. Rising claims severity, expanding litigation, and the compounding effect of unsafe driving behaviors have made reactive risk management an unsustainable strategy—and the numbers bear that out.

Telematics in insurance is a viable path forward to sustained profitability for commercial auto. Not because it is a new technology, but because the industry has reached the maturity, adoption, and analytical capability to deploy it at scale and measure its impact with precision. The data infrastructure is largely in place. The proof points are established. What remains is execution, and that starts with solving the fragmentation problem that prevents telematics data from reaching its full potential.

SambaSafety has spent over 25 years building driver risk intelligence with that exact challenge in mind. By integrating with 100-plus telematics service providers, their platform normalizes fragmented data from across the TSP landscape into a single, actionable driver risk profile.

From that unified profile, the platform connects risk signals to intervention. This is what telematics in insurance looks like when fully operationalized. Not a dashboard to check occasionally, but a continuous workflow in which monitoring, intervention, and outcome measurement are connected end to end. For insurers and brokers evaluating how to build or scale a telematics strategy, the architecture of that workflow matters as much as the data itself.

-1.png)