IBNR (Incurred but Not Reported) sits at the intersection of actuarial science and market reality. With today’s unpredictable commercial auto environment, getting IBNR wrong isn’t a rounding error, but a potential multi-billion-dollar problem.

Most insurance professionals know what IBNR is, but far fewer are talking about what it’s doing to commercial auto insurance right now. A number worth acknowledging? AM Best estimates commercial auto liability is under-reserved by $4-5 billion. The industry built that gap slowly, through underestimated severity, longer litigation timelines, and a reserving concept it continues to treat as a lagging rather than a leading indicator of risk.

IBNR isn’t a footnote, however. It’s a mechanism through which years of inadequate loss estimates quietly turn into balance sheet crises. For an insurance market that has lost money for 14 consecutive years, understanding IBNR is becoming increasingly essential to navigating the path forward towards profitability.

IBNR Meaning: What It Is and How It Works

IBNR is an insurer’s best estimate of liability for losses that have already occurred but haven’t been reported or resolved yet. Insurers rarely know how many unreported claims are coming or how large they’ll be, so actuaries project that number based on historical patterns and professional judgment.

The reason IBNR estimates can go sideways, especially in commercial auto, comes down to what’s accurately being estimated. Two distinct components make up the total number:

-

Incurred but Not Yet Reported (IBNYR), also called “pure IBNR,” is a subset of IBNR that accounts for unpaid liability for claims that occurred by the evaluation date but have not yet been reported to the insurer. For example, this could be a crash victim who hasn’t filed yet or a claim still in transit. The insurer knows the loss exists in aggregate, but not the details.

-

Incurred but Not Enough Reported (IBNER) is a type of IBNR designed to recognize any deficiencies or redundancies in individual claim reserves. It reflects losses that have occurred, but the individual claim reserves are not enough to account for the overall estimated unpaid claim liability. For example, if a claim is first reserved at $50K and ultimately settles for $400K, that $350K gap is IBNER. In commercial auto, this is often the larger and more volatile of the two because it’s hardest to predict with today’s litigation environment.

On a balance sheet, IBNR sits as a liability. Combined with case reserves on known open claims, it forms an insurer’s total loss reserves, which is typically the largest single liability on the books. What makes IBNR more than an accounting entry is its close connection to reported earnings. When actuaries set it too low, strengthening those reserves becomes an acknowledgment that earlier estimates fell short.

As losses develop beyond original estimates, that gap doesn’t stay quietly on the balance sheet. It hits current incurred losses, regardless of when the underlying accident actually occurred. The result is a combined ratio that continues to deteriorate long after the policy year closes.

How IBNR Connects to Combined Ratio

The combined ratio is how the insurance industry measures underwriting profitability. It adds the loss ratio (claims paid relative to premiums earned) to the expense ratio, the cost of running the business. A combined ratio below 100% means the insurer is making money on underwriting. Above 100%, and the insurer is losing money on every underwriting dollar, before investment income counts for anything.

IBNR sits at the center of that equation because incurred losses capture more than what’s already been paid. They include case reserves on open claims and IBNR reserves for losses that haven’t fully emerged yet. That means every time IBNR is revised, incurred losses move with it. And when incurred losses move, so does the loss ratio. And when the loss ratio moves, so does the combined ratio.

The most consequential way this plays out is through prior-year reserve development. When actuaries determine that IBNR from a prior accident year was set too low, they strengthen reserves in the current period. That catch-up is booked as additional incurred losses today, even if the underlying accident happened two or three years ago. It’s one of the more counterintuitive dynamics in insurance: a policy year can look reasonably profitable when it closes, then quietly deteriorate over years as claims exceed initial estimates.

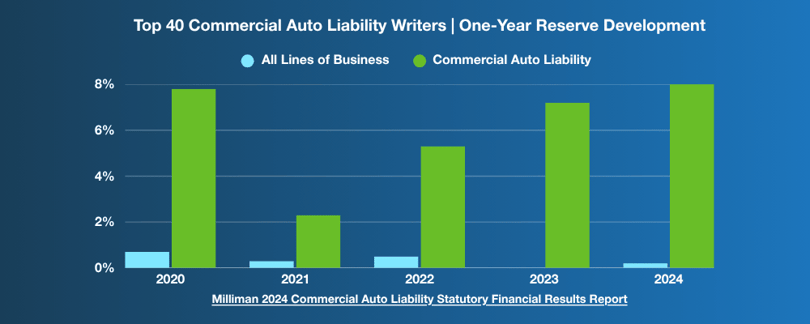

In commercial auto, that deterioration has been anything but quiet. According to Milliman's research, prior-year reserve development for commercial auto liability continues to be adverse, with 2024 showing 8.0% one-year reserve development. The pattern is consistent: insurers set IBNR; losses develop worse than expected, reserves get strengthened, and the combined ratio takes the hit; year after year, on top of losses that are still actively accumulating from current business.

That’s not a reserving problem in isolation. It’s a signal that the underlying risk is changing faster than historical data can capture—and that’s exactly what’s happening in commercial auto right now.

Why IBNR Is So Hard to Get Right Today

A confluence of factors has made it difficult for insurers to get IBNR correct the first time. Three key forces at play are nuclear verdicts, social inflation, and commercial auto loss dynamics.

-

Nuclear verdicts are distorting severity distributions. In 2024, Marathon Strategies reported 135 nuclear verdicts exceeding $10 million—a 52% increase from the prior year. Because actuarial models rely on historical severity distributions to project ultimate losses, when the tail of that distribution suddenly produces outcomes three or four times larger than anything in the historical dataset, the traditional factors used become structurally inadequate.

-

Social inflation is systemically inflating claim costs. Average loss severity for commercial auto liability has nearly doubled over the past nine years at an average annual rate approaching 8%, far outpacing economic inflation of roughly 3%. Third-party litigation funding is accelerating this trend by enabling claimants to sustain longer, more aggressive litigation.

-

Long-tail dynamics compound the estimation problem. Complex commercial truck cases can take one to three years in active litigation, and with appeals, full resolution can extend well beyond that. At the end of 2023, reserves per outstanding commercial auto liability claim were $61,000—37% higher than the year-end 2019 level. The longer a claim stays open, the more time there is for severity to drift further from the original estimate.

These factors can help insurers understand why IBNR continues to deteriorate in commercial auto insurance. Still, it’s only half of the equation. The same market dynamics that make it difficult to get IBNR right also point toward where the solutions lie.

The insurers gaining momentum aren’t just refining their actuarial models; they’re going after the underlying risk that makes accurate IBNR estimation by reducing the frequency and severity of the losses that drive reserve uncertainty before those losses can ever show up on the balance sheet.

What Better IBNR Management Looks Like

There’s no one fix to improving IBNR accuracy. But some practices separate insurers who get ahead of reserve development from those who are perpetually surprised by it.

It starts with methodology. The most agile insurers don’t rely on a single actuarial method; they run several in parallel and compare the results based on which assumptions hold in the current environment:

-

Chain ladder is the most widely used approach because it looks at how claims have developed historically and projects that same pattern in the future. However, when social inflation is actively pushing severity higher, that assumption fails, and IBNR ends up undervalued.

-

Bornhuetter-Ferguson takes a more balanced approach by blending historical patterns with an estimate of what losses should look like, making it more stable in recent accident years when few claims have emerged yet and less vulnerable to being thrown off by a handful of early, large losses.

-

Frequency-severity breaks the estimate into expected claim count and average cost per claim. In commercial auto, where severity is the dominant driver of reserve pressure, this method helps pinpoint whether the problem is more claims, more expensive claims, or both.

Beyond methodology, data quality is foundational. Any IBNR estimate is only as reliable as the data behind it. Leading insurers are moving toward continuous monitoring rather than waiting for quarterly or annual reserve reviews to surface problems.

But the most durable path to IBNR accuracy is something that actuarial methods alone can’t deliver: reducing the underlying risk. Every crash that doesn’t happen is an IBNR reserve that never needs to be set. Every high-risk driver identified and coached before an incident is a severity event that actuaries never have to model.

This is where telematics and continuous driver monitoring have become increasingly relevant to the reserving conversation. According to SambaSafety, fleets that combine telematics with targeted driver training have reduced violations by an average of 77% within 12 months. Multi-year studies show a 22% reduction in claims frequency and a 50% reduction in bodily injury claims—the claim type most likely to develop into the severe, litigated cases that create IBNR uncertainty in the first place. For commercial auto insurers, policyholders who actively manage driver risk don’t just produce better loss ratios. They produce more predictable loss development, which means the IBNR estimates set at policy inception are far more likely to hold.

What Is the Cost of Getting It Wrong?

Despite most insurance professionals knowing what IBNR is, few are acting on its implications. Nuclear verdicts, social inflation, and long-tail development don’t show up on the balance sheet the day they occur. They surface months or years later, quietly through reserve strengthening, adverse development, and combined ratios that have no obvious connection to what’s happening in the current book. That’s the cost of treating IBNR as a back-office calculation rather than a live risk signal.

The insurers who emerge from this cycle strongest are those who close that gap—investing in better reserving methods, better data infrastructure, and programs that reduce the frequency and severity of the losses driving reserve uncertainty in the first place.

The $4–5 billion reserve deficiency AM Best has identified didn’t appear overnight, and won’t be resolved by pricing alone. Insurers that combine sophisticated reserving with proactive risk reduction are building books that are not only better priced—they’re more predictable. That means better risk selection at the front end, giving underwriters comprehensive driver risk data to price accurately before a policy is bound.

It means continuous visibility throughout the policy term, equipping loss control teams with driver monitoring and portfolio insights to catch emerging risks before they become claims. And it means helping policyholders actively manage their fleets through targeted training and telematics data, so that loss development becomes more predictable and IBNR estimates are more likely to hold.

That’s what better IBNR looks like in practice, and SambaSafety can help you get there.

-1.png)